Private Label Reinforces Its Strong Presence Across Europe

The private label share across 17 countries in Europe is growing according to the data of NielsenIQ. The share grew to 38.8% based on MAT W52 2025 (+0.33%pnt versus MAT W52 2024). NielsenIQ surveyed 17 markets for PLMA’s 2025 Private Label Market Report and noticed an increase for retail brands in 12 out of the 17 countries.

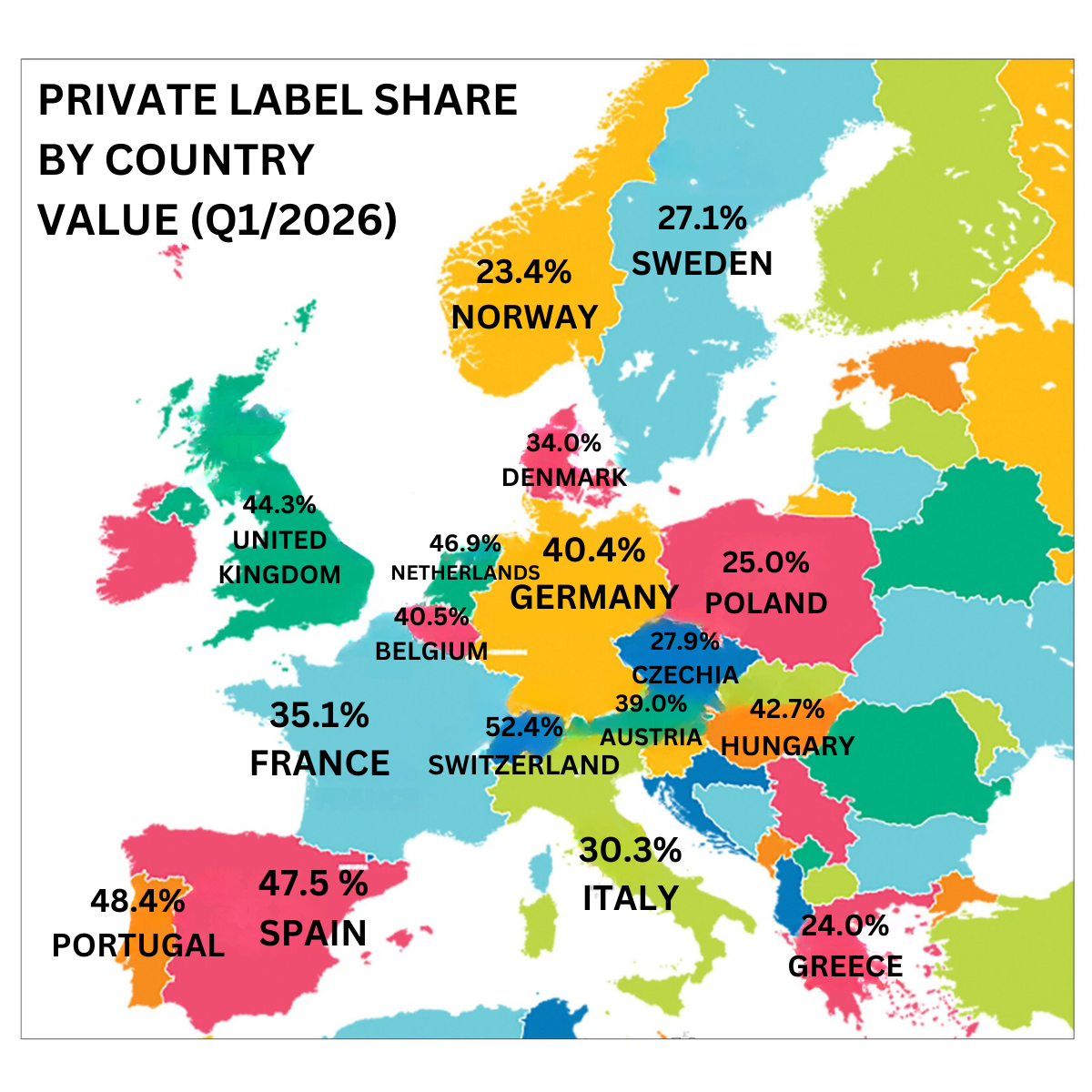

European markets remain some of the biggest Private Label markets globally. Twelve markets now report private label shares above 30%, while eight markets exceed 40%. The country with the highest share across the 17 countries tracked is Switzerland, with 52.4% making it is the only country with a value share above 50%, representing more than €14 billion.

Country-Level Performance

The strongest growth in private label share was recorded in:

• Spain: +1.0%pnt

• Austria: +0.9%pnt

• Portugal: +0.7%pnt

• The Netherlands: +0.4%pnt

Europe’s largest markets, Germany, United Kingdom and France, have a collective Private Label share of 40.4%, this share grew +0.2%pnt vs last year. The highest share growth for the largest markets is visible in Confectionery & Snacks and Perishable Food.

Spain and Portugal gained Private Label share by +1.0%pnt. The highest share growth is visible in Home Care which grew +1.8%pnt. In Spain and Portugal Pet Food (-1.1%pnt) and Alcoholic Beverages (-0.01%pnt) are declining in share.

In Belgium and The Netherlands, the private label share increased by +0.2%pnt. The highest growing category is Confectionery & Snacks by +0.8%pnt. However, more than half of the categories continue to decline with Pet Food (-1.8%pnt), Home Care (-1.1%pnt) and Alcoholic Beverages (-0.4%pnt) taking the lead.

In Eastern Europe the private label share is growing (+0.2%pnt). The highest growth in private label share is visible in Ambient Food (+1.3%pnt), Health Care (+1.2%pnt), and Frozen Food (+0.7%pnt) while Pet Food is declining the strongest (-2.0%pnt)

The Scandinavian countries increase in the Private label share (+0.1%pnt). The highest growing category is Confectionery & Snacks by +0.3%pnts. However, more than half of the categories decline in Private label share with Pet Food (-1.3%pnt) taking the lead.

According to NielsenIQ’s data, Confectionery & Snacks, Food Ambient, and Perishable Food are the top 3 categories of Private Label value share with an average of 48.4% representing, in total 261 billion Euros across the 17 European countries tracked. Overall, the private label sales grew with 14.8 billion euros across the 17 European countries tracked.

Private label products encompass all merchandise sold under a retailer's brand. That brand can be the retailer's own name or a name created exclusively by that retailer. In some cases, a retailer may belong to a wholesale group that owns the brands that are available to only the members of the group.

Major supermarkets, hypermarkets, drug stores and discounters offer products under the retailer's brand. Private label covers lines of fresh, canned, frozen, and dry foods; snacks, ethnic specialties, pet foods, health and beauty, over-the-counter drugs, cosmetics, household and laundry products, DIY, lawn and garden, paints, hardware, auto care.

For the consumer, private label represents the choice and opportunity to regularly purchase quality food and non-food products at savings compared to manufacturer brands, without waiting for promotional pricing.

Private label items consist of the same or better ingredients than the manufacturer brands, and because the retailer's name or symbol is on the package, the consumer is assured that the product meets the retailer's quality standards and specifications.

Manufacturers of private label products fall into three classifications:

• Large manufacturers who produce both their own brands and private label products.

• Small and medium size manufacturers that specialise in product lines and concentrate on producing private label almost exclusively.

• Major retailers and wholesalers that operate their own manufacturing plants and provide private label products for their stores.